[ad_1]

Joe Raedle

Carvana Co. (New York Stock Exchange: CVNA) is an Arizona-based company with a market capitalization of $7.5 billion that operates a US-based e-commerce platform for buying and selling used cars. Customers can research, inspect, finance and purchase vehicles online, with delivery or pickup options.

Yeah If you take a quick look at the plethora of short-rated articles here on Looking for Alpha, you’ll immediately understand that there are a few problems with CVNA: Multiple analysts can’t rate it “Sell” from quarter to quarter, and do so repeatedly. . And meanwhile, CVNA stock is up a whopping 790% year to date:

Looking for Alpha, CVNA

This behavior is explained by the abundance of open short positions that must be closed at some point, which causes a kind of domino effect in the trading order book. [aka DOM] when short sellers, to cover losses, are forced to close at any market price, causing the stock to ever higher price. Excuse this “brief squeeze” explanation, I just wanted to make sure all readers understand the reason for such a steep increase in CVNA’s price.

Although CVNA has already experienced such strong growth so far this year, its popularity among short sellers continues unabated. And I’m not even talking about retail speculators, but solid Wall Street suits, for whom CVNA remains the prime candidate for short positions, according to the latest Goldman Sachs data I found. [August 21, 2023 – proprietary source]:

![Goldman Sachs [August 21, 2023]](https://static.seekingalpha.com/uploads/2023/8/26/49513514-16930391933728004.png)

Goldman Sachs [August 21, 2023]

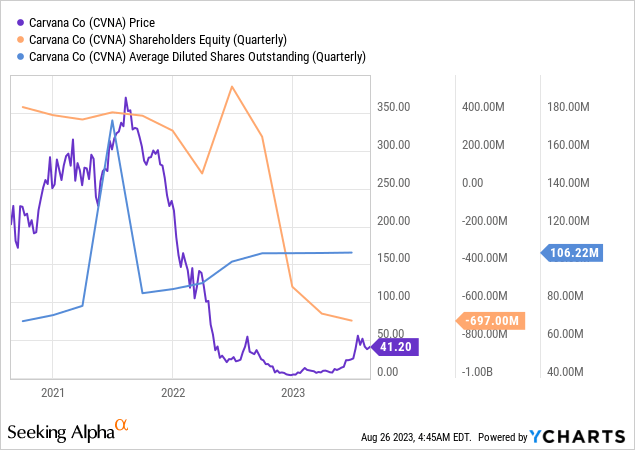

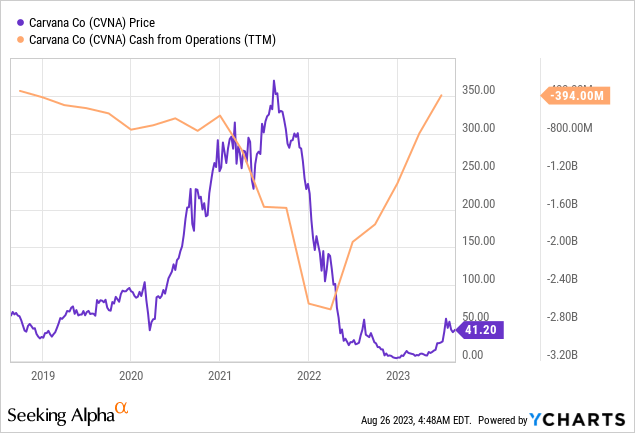

Throughout its history, Carvana has spent significant investment capital to fuel growth, but has never achieved consistent profitability or generated positive cash flow. What he achieved was to burn the stockholders’ equity and issue more shares.

Kerrisdale Capital’s CVNA article dated June notes that even during the pandemic, when it was one of the few online options for car buyers, Carvana was unable to turn a yearly profit. Faced with the risk of bankruptcy, the company tried to reduce costs and streamline its operations, but was still unable to generate positive cash flow from operations.

Carvana now tries to promote a new narrative. During the last earnings conference call, the CEO outlined a three-step plan the company undertook: achieve positive adjusted EBITDA, achieve positive unit economics, and then return to growth.

But in reality, CVNA still faces some very crucial challenges: The used car business, whether traditional or technological, is capital intensive and low margins.

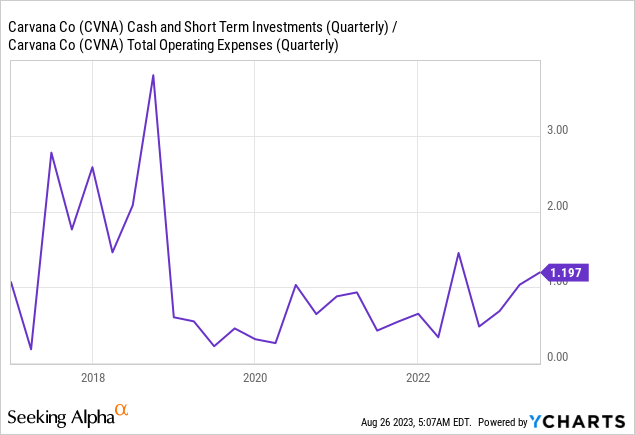

Yes, CVNA has actually managed to slightly reduce its operating expenses and cost of goods sold (as a percentage of sales) in recent quarters, resulting in a positive adjusted EBITDA margin. However, given the peculiarities of the industry in which the company operates, it is very likely that it will have trouble sustaining the recent margin expansion.

YCharts, author’s notes

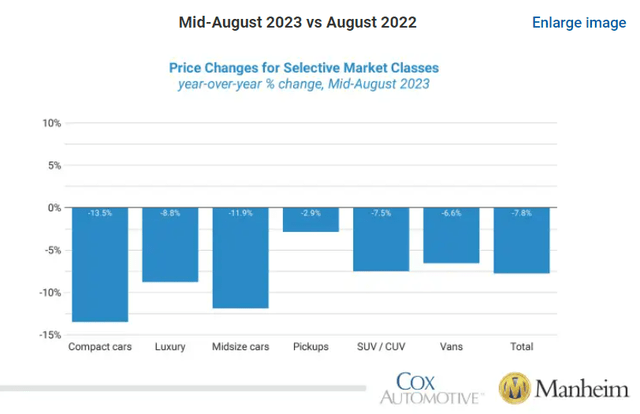

Even under favorable conditions like low interest rates and high used car prices, Carvana did not prosper. With the current unfavorable conditions and its significant debt, the company’s only viable option is likely to eventually be to restructure its financial obligations.

Used Vehicle Value Index, Manheim

graphs and

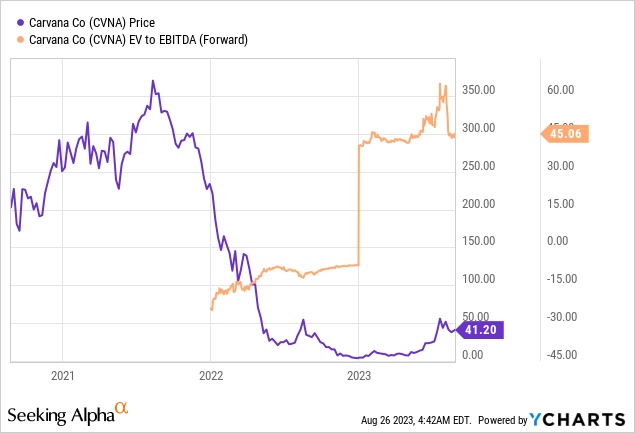

Just over a quarter of the cash expense remains on the company’s balance sheet [in the form of operating expenses]. From a historical perspective, this is not a problem for the company: the graph below clearly shows that this is not the first time that CVNA has faced a liquidity problem. However, in the past, this problem has been solved by further debt and equity increases. After such a sharp rise in shares, the second option is more likely this time.

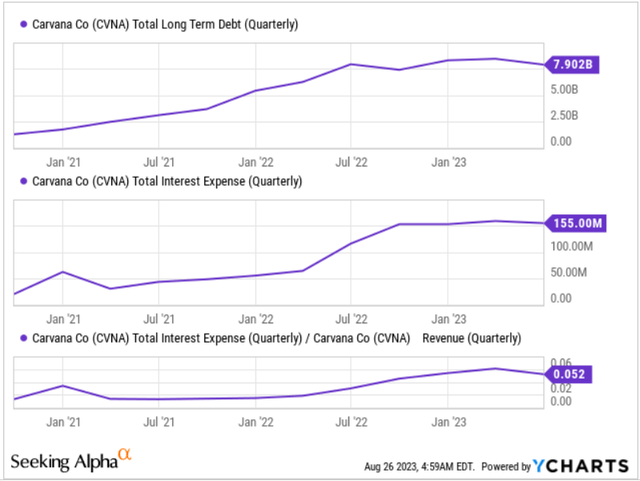

Is it worth talking about how high CVNA shares began to value after the price growth to date? Right now, any buyer of CVNA stock is willing to wait about 45 years for EBITDA, and that’s despite the company’s value being significantly inflated by debt that none of the banks are likely to refinance at a rate of attractive rate (taking into account the recent rise in nominal interest rates).

So from a purely fundamental perspective, CVNA is itself a huge red flag for investors. But the problem is that this thesis is clear to everyone.

Not only because short-term interest exceeds 40-50%. Everyone is aware that sooner or later the fundamentals will set in, but no one knows exactly when it will. This is why many short sellers keep coming back to CVNA and try to sell it again, thinking that it has already peaked. The bitter truth is that such attempts often end in painful failure. To avoid this, short sellers must take into account the relative strength of the stock and wait until it weakens.

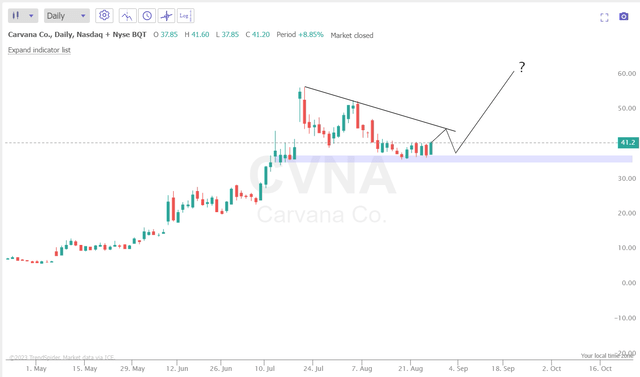

In general, I think that we are still in a euphoric phase where it is not worth trying to seize the moment to go short. While the price on the weekly chart has fallen from its previous local resistance in the $50/sh area. The pressure can still continue.

TrendSpider software, author’s notes

Some banks now rate CVNA a “buy,” according to TrendSpider data, which could paint a favorable picture for growth “against fundamentals” given high short-term interest and likely more positive news from the company.

On the other hand, could it be that the rejection of the resistance zone is exactly in line with the seasonality we have seen in CVNA price action over the last 6 years, where September and October have been the most painful for growth? ?

The answer is: no one knows.

Anyone who wants to sell CVNA at the current price level risks losing their capital if the current technical landscape continues to develop as technical analysis textbooks teach: Consolidation after breakout – new breakout:

TrendSpider software, author’s notes

On the other hand, buying CVNA is speculation, not a balanced long-term investment decision. That’s because of the CVNA. [in my humble opinion] the lousy finances, the struggling industry and the outrageously high valuation, which will inflate sooner or later anyway.

Therefore, I advise speculators to wait for more signs of exhaustion of the current rally before shorting, and long-term investors to avoid these meme stocks altogether.

Thank you for reading!

#Carvana #Stock #Simple #NYSECVNA