[ad_1]

Meletios Verras

If you want something new, you have to stop doing something old.-Peter Drucker

Today, we take a look at a development company that finds itself deep in failed IPO territory. However, the stock has experienced some recent buying by a The ultimate beneficiary has some key test readings on the horizon. An investment analysis is presented below.

looking for alpha

Company Overview:

AlloVir, Inc. (NASDAQ:ALVR) is a Waltham, Massachusetts-based clinical-stage biotechnology company focused on the development of allogeneic (donor) T-cell therapies to treat viral diseases. The company’s leading commercially available virus-specific T cell [VST)] The program is posoleucel, which is being evaluated in three phase 3 trials with a fourth likely to start in the next twelve months. AlloVir was founded in 2013 as AdCyte (later ViraCyte) and went public in August 2020, raising net income of $292.0 million at $17.00 per share. The stock is trading around $3.00 per share, which translates to a rough market. cap of 335 million dollars.

The company is a subsidiary of ElevateBio, whose raison d’être is to leverage its cell and gene therapy manufacturing capabilities into ownership stakes in companies like AlloVir, a sort of hedge fund hotel for biotech. As part of its 2018 deal, ViraCyte (now AlloVir) issued preferred shares to ElevateBio and other affiliate investors that converted into 39.9 million common shares at its IPO. In exchange, AlloVir received $156.3 million in pre-IPO financing and gained access to ElevateBio’s gene and cell therapy manufacturing facilities (known as Base Camp). In fact, the relationship is such that AlloVir shares the same president, CFO and various board members with ElevateBio, which still holds an 18% stake in the company.

Platform

AlloVir’s platform is designed to produce cell therapies that restore VST immunity and eliminate active viral infections.

In healthy individuals, the adaptive immune system produces CD8+ T cells that kill virus-infected cells, as well as CD4+ T cells that produce cytokines, support CD8+ cells, and signal other aspects of the immune system to amplify the overall response. T cells recognize a virus-infected cell through a specific human leukocyte antigen (HLA) receptor present on its outer surface. Once bound to the HLA receptor complex, the T cell multiplies and migrates to other virus-presenting cells to control or eliminate the infection. HLA composition is different from human to human, but there are only a limited number of unique HLA types (such as blood types) that make T-cell donation feasible.

The company’s first opportunity is the ~40,000 patients who receive an allogeneic hematopoietic cell transplant (allo-HCT) annually for blood cancers, blood disorders and other immunodeficiencies. Prior to this procedure, the patient’s immune system must be eradicated in order to generate the graft of donor cells. As such, after allo-HCT, it can take up to a year for a patient’s adaptive immune system to return to normal function. Meanwhile, the body is extremely vulnerable to viral infection, and up to 70% of allo-HCT recipients develop a clinically significant infection (CSI) that can fuel disease morbidity and mortality. The same dynamic applies to solid organ transplants.

Company website

Enter AlloVir’s VST manufacturing platform, which uses T cells from donors who are seropositive for specific viruses. It then mass-produces the VST polyclonal output ex vivo. The T cells are then filtered through another algorithm to match the HLAs with specific profiles of each patient, and are then introduced into that patient. The entire process takes approximately two weeks and hundreds of doses of VST are produced from a single donor. To date, the company’s platform has generated two clinical assets.

Company website

Pipeline:

Company website

posoleucel. AlloVir’s main program is posoleucel (formerly known as Viralym-M or ALVR105), which is a commercially available allogeneic VST that targets six common viruses: adenovirus (AdV), BK virus {BKV}, cytomegalovirus (CMV) , Epstein-Barr virus (EBV), human herpesvirus 6 (HHV-6), and JC virus (JCV). It is being evaluated in three Phase 3 studies: one for the treatment of virus-associated hemorrhagic cystitis (HC}, one for the treatment of AdV infections, and one for the prevention of multiple ICS due to multiple viruses. The first two trials cover patients who develop a CSI; third study involves posoleucel in a preventive setting. All three should complete enrollment by year 23 and provide data by mid-2024.

Company website

Optimism about the results of these studies is supported by the Phase 2 results. In particular, in the phase 2 CHARMS proof-of-concept study with 58 company patients (read December 2020), 95% of allo-HCT recipients had infections with one or more of the target viruses and failed or were intolerant of conventional ones. antiviral treatment, achieved a clinical response with posoleucel at week 6 without cytokine release syndrome. In a separate phase 2 study for the prevention of multiple viruses, 88% of patients (23/25) remained free of ICS caused by any of the six viruses targeted by posoleucel through week 14.

Company website

Additionally, in a phase 2 solid organ (kidney) transplant study, posoleucel achieved greater viral load reduction compared to placebo across all BK viral load measures, with responses increasing over time. The treatment effect was most pronounced in patients with high viral load who received biweekly doses, where a viral load reduction of at least one log was achieved in 75% of patients (12/16) vs. 25% (1 /4) of those who received placebo. This essay, read in February 2023, will help inform a pivotal study when AlloVir meets with the FDA, which is expected to occur sometime in FY23.

AlloVir’s lead candidate has received Regenerative Medicine Advanced Therapy (RMAT) designations for the treatment of HC caused by BKV after allo-HCT; AdV infection after allo-HCT; and for the prevention of CSI and end-organ diseases of the six target viruses after allo-HCT. It has also received EMA PRIority Medicine designation for the treatment of severe infections caused by five of the six targeted viruses, as well as an Orphan Drug designation for targeted viruses in HCT patients.

ALVR106. AlloVir’s other clinical candidate is ALVR106, a commercially available allogeneic VST that targets diseases caused by four respiratory viruses: human metapneumovirus; influenza; parainfluenza; and respiratory syncytial. It is being evaluated in transplant patients in a proof-of-concept study currently enrolling patients in the US.

Company website

Stock Price Performance

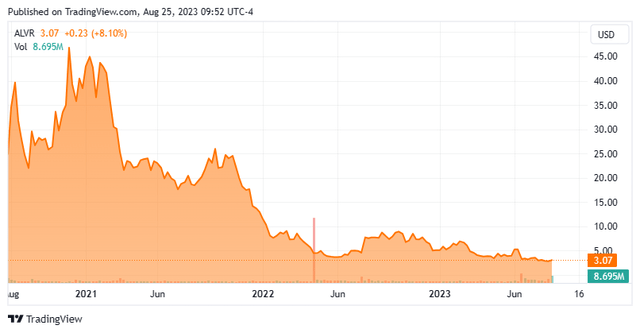

With plenty of RMAT designations and clinical trials, but relatively little major data since the CHARMS read in December 2020, the company burned through cash without another significant catalyst to propel it higher. It’s not that subsequent multiviral or kidney transplant studies weren’t positive, they just weren’t momentous. When we last looked at AlloVir in October 2021, its shares were trading at $24.72 per share and it had cash of $313.3 million, but that only provided an operating clue through fiscal year 23. Knowing that the company would have to return to the capital markets and with little clinical data to boost its share price, the market slowly pulled away. AlloVir waited too long to return to seek funding, eventually netting $126.4 million at $4.61 per share through a private placement in July 2022. However, with no results from its Phase studies 3 until mid-2024, the company was forced once again. to conduct highly dilutive financing, raising net proceeds of $81.1 million (assuming a greenshoe exercise) at $3.75 per share in a secondary offering priced on June 21, 2023.

Balance Sheet and Analyst Commentary:

These two post-IPO capital increases have increased the number of AlloVir shares by more than 50 million, bringing its total to 116.6 million (78% dilution). That being said, cash and short-term investments (as of June 30, 2023) are ~$250 million, providing the company with a cash trail through early 2025.

Over the past month, Piper Sandler ($27 price target), Morgan Stanley ($20 price target) and Bank of America ($18 price target) have reissued or assigned Buy ratings on the stock.

In addition to ElevateBio, Gilead Sciences (GILD) has a significant stake in the company. His former head of virology, Diana Brainard, is now the CEO of AlloVir. In the recent secondary, Gilead bought 2.93 million shares, keeping its stake above 14%.

Verdict:

Despite AlloVir’s ill-timed capital increases, it is in a rather enviable competitive position. First, there are currently no FDA-approved cell therapies for the viral diseases targeted by posoleucel, although Atara Biotherapeutics (ATRA) Ebvallo (tabelecleucel) received European marketing authorization for the treatment of EBV-associated post-transplant lymphoproliferative disease in December 2022 and is expected to provide an update on a BLA submission in 3Q23. Other than Ebvallo, the only other approved remedies for any of the viruses targeted by posoleucel are antiviral drugs targeted at CMV disease, which are associated with significant toxicity. Vera Therapeutics (VERA) MAU868 was scheduled to enter the phase 3 study for the treatment of BKV in kidney transplant patients, but was recently deprioritized.

Since enrollment in its three Phase 3 trials will end by year 23 and posoleucel produces results similar to Phase 2 results by mid-2024, there is a path toward approval and launch of at least one indication (if no more) before the 25th year. With more than 40,000 HCT performed annually worldwide, posoleucel has the potential for great success before the solid organ transplant opportunity is seized. As such, with the company valued at ~$100 million net of cash, it’s worth a little ‘see article‘ The investment, as its shares should gain momentum in the Phase 3 readings of mid-2024.

Our miserable species is made in such a way that whoever walks the beaten path always throws stones at whoever shows him a new path..”—Voltaire

#AlloVir #Stock #Intriguing #Biotech #Concern #NASDAQALVR