[ad_1]

huber and starke

California regulators voted Thursday to allow Cruise (NYSE: GM) and Waymo (GOOG) (GOOGL) to begin operating a 24/7 paid taxi service in San Francisco. Anyone who has been to the city of Recently, in San Francisco, especially at night, cars have been seen driving by, strangely with no one in the driver’s seat. Many of them have been operating as taxis, leading to some unique results.

As we will see throughout this article, autonomous driving is a new investment opportunity; however, we expect there to be significant winners and losers in this risky new industry.

The autonomous driving problem

The problem of autonomous driving is enormously complex. Because regardless of what some media outlets may lead you to fear, general AI doesn’t exist yet. Computers follow a set of rules. Modern statistics, combined with extraordinarily complex rules, lead to an AI that seems to seem extraordinarily complex, like GPT Chat.

In fact, the impacts on training data of the growing number of generative AI models have made current generative AI worse. Autonomous driving is a complex set of rules and when it encounters an unexpected scenario it fails. As a result, we expect AI to continue as Cruise and Waymo are developing it: city-level robotaxis that earn revenue and collect data.

Market opportunity

The market opportunity is huge.

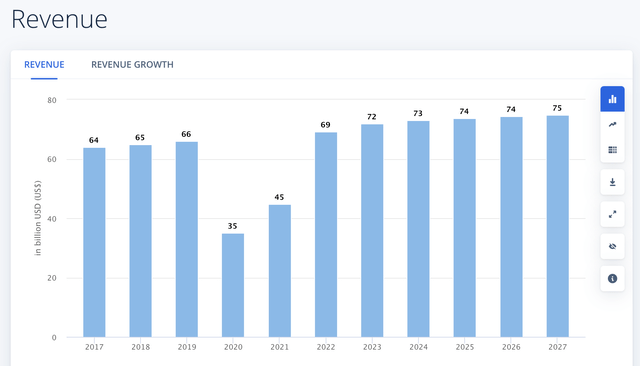

taxi revenue

The revenue earned from private transport and taxi services is clearly enormous. Despite a sizable drop during COVID-19, industry profits will exceed $70 billion this calendar year. The city model allows these companies to take advantage of major markets to start that are responsible for a substantial percentage of the market, such as New York or San Francisco.

Since Waymo and Cruise are already taking advantage of the market, making cold hard cash as they improve, they are already taking advantage of the market.

Leverage

So what is the best way to take advantage of this? Cruise currently has twice the fleet size of Waymo: Cruise has about 400 vehicles and Waymo has about half as many. However, Waymo runs better 24/7, while Cruise runs mostly at night, showing potential fear for the intensity of daytime operations.

The answer is, it depends.

General Motors (NYSE: GM) has a market capitalization of $46 billion with its 80% ownership in Cruise. Waymo was once worth nearly $200 billion, but is now worth $30 billion. It is estimated that the value of the cruise is about 30,000 million dollars. That means it accounts for just over half of General Motor’s valuation. Clearly, any success there would be very profitable for General Motors.

On the other hand, Google is huge. It is worth almost 1.7 trillion dollars. That means that even if Waymo is worth several hundred billion dollars, the advantage for Google will be much smaller. Of course, if Waymo never gets anywhere, Google’s core business and current value is far less important than Cruises.

The investment you take advantage of is based on your personal risk profile and the amount of exposure you want to the autonomous results of that company.

The Tesla Downside

Let’s get to our take on one of the most talked about companies in the world of autonomous driving, Tesla (NASDAQ: TSLA).

Tesla’s focus appears to be increasingly focused on driver assistance rather than fully autonomous driving. The company has plenty of miles in its systems, but it hasn’t begun to implement fully autonomous driving without a driver like Cruise and Waymo. They may have statistics on the human interventions required, but they don’t take advantage of all the unique opportunities that occur when human drivers don’t use the system as much, such as driving in complex, short-distance cities.

Cruise and Waymo have made constant interventions, but each time they learn something from them. They are already earning revenue from the business and collecting data. We believe Tesla trails Cruise and Waymo by a significant margin in terms of fully autonomous driving revenue. At this point, Tesla hasn’t indicated any kind of path to get to where Cruise and Waymo are, that’s more of a long-term goal.

There is something else worth noting here that is coming more and more into view. Regulatory burden. Autonomous driving was allowed 24/7 in San Francisco after years of testing and despite strong protests. Some would say that if it had been a San Francisco decision and not a California regulatory decision, it would not have passed at all. Each city is a complicated process that requires years of effort and planning.

The path to autonomous vehicle revenue appears to be the replacement of taxis in major cities, something that can be thoroughly researched and mapped. They have the scale to make that effort worthwhile. More importantly, Waymo and Zoox are backed by companies that can spend tens of billions of dollars to make it happen. Cruise is already a leader and General Motors is strong. Tesla is behind and even as a car company it is not profitable enough to continue these investments on a larger scale.

With autonomous driving being a key part of Tesla’s incredibly high valuation against other automakers, we expect it to underperform as it continues to fall behind in the race.

our view

Humanity is great and the problem solving and the amount of money being invested here along with the start of regulatory approval means they believe there is a way forward.

However, there are winners and losers and levels of risk. Google is the classic option. His technology seems to lead, on road issues, against Cruise. You have the financial backing to keep investing heavily, and even if the business ends up worthless, you’re not in particularly difficult straits with your investment.

General Motors is a higher risk, higher reward company. Cruise is doing incredibly well with his growing stream of robotaxis. The company makes up a sizeable chunk of General Motor’s valuation, meaning it has the potential to reap far greater shareholder rewards if it succeeds. However, General Motors’ core business still helps provide useful insulation.

Then there is Tesla. The company is dramatically overvalued, and one way to achieve that would be an incredibly successful self-driving business, but it’s not leading that way. We expect Tesla to continue to struggle to justify its valuation, and as it falls, the chances of investors taking notice increase, punishing it further.

thesis risk

In our opinion, the biggest risk to the thesis is an unexpected technological balance, a “gold nugget” that happens from time to time. Tesla could have one, some moment of technical genius, that changes the field. It has happened before in AI with the creation of generative AI models and more. Tesla is actively investing and could make a breakthrough that allows it to catch up with its competitors.

#Autonomous #driving #San #Francisco