[ad_1]

MediaProduction/iStock via Getty Images

AMD’s investment thesis remains strong, but only for the patient

We previously covered Advanced Micro Devices, Inc. (NASDAQ:AMD) in May 2023, rating the stock a Buy, with strong demand for generative AI it will likely trigger the next semiconductor supercycle.

We also believed that the strategic leadership of CEO Lisa Su and Victor Peng (formerly of Xilinx) could eventually enable AMD to close the gap with Nvidia (NVDA), thereby resulting in the expansion of revenue and profits from the first .

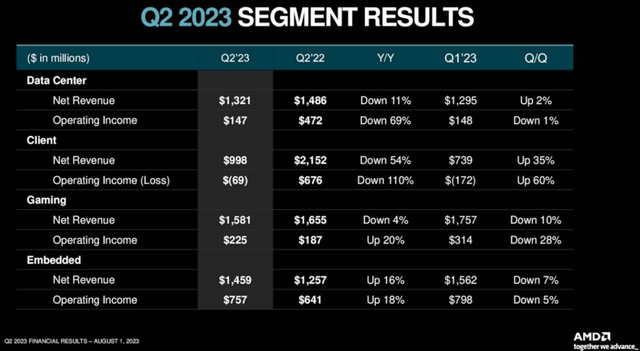

AMD FQ2’23 Performance

looking for alpha

For now, thanks to NVDA’s stellar performance in Q2 2024, with data center sales of $10.32 billion (+141.1% QoQ/ +171.5% YoY), representing 76 .3% of its overall total revenue (+16.8 qoq/ +19.6 YoY), it’s clear that AMD investors are momentarily in the mood.

AMD reported disappointing data center revenue of $1.32 billion (+2.3% qoq/ -10.8% yoy) in the same quarter, suggesting that NVDA has eaten everyone’s lunch, as similarly observed multiple market analysts.

Most importantly, AMD’s data center segment operating margin of 11.1% (-0.3 points QoQ/ -20.6 points YoY) has also fallen sharply, with its overall inventories at $4.56 billion ( +7.8% qoq/ +72.7% yoy) which remain inflated in the second quarter. ’23.

Consumer demand for AMD’s latest EPYC Bergamo CPU also doesn’t appear to be impressive, with the company slashing MSRPs by as much as -20%, despite the cloud-optimized processor’s claimed market-leading performance.

This is in stark contrast to NVDA’s growing gross margins of 70.9% (+6.3 points QoQ/+25.6 YoY) and operating margins of 51.4% (+21.6 points QoQ/+41 .3 yoy) in the last quarter, implying solid consumer demand despite the price premium.

AMD’s Q3 2023 revenue guidance of $5.7bn (+6.5% qoq/+2.5% yoy) also does not inspire confidence, attributed to slower sampling of the MI300 in Q3 of 23 and to increased production only in the fourth quarter of 23.

Whether AMD’s MI300 chip accelerator is able to significantly gain some of NVDA’s current market share remains to be seen, especially given the latter’s massive Q3 2023 revenue guidance of $16 billion ( +18.4% quarterly/+169.8% year-on-year).

Assuming a similar cadence in Q2 2023, we can extrapolate a higher data center weight of $12.2bn in Q3 2023 (+18.2% QoQ/+218.5% YoY), suggesting another massive GPU win for Jensen Huang and to a lesser extent Intel (INTC) as the DGX H100 uses Sapphire Rapids CPUs.

NVDA’s impressive growth is naturally attributed to “accelerating demand from cloud service providers and large consumer Internet companies for the HGX platform, generative AI engine and large language models, based on our Tensor GPUs.” Core of Hopper and Ampere architecture”.

Uncertain compatibility issues may also affect whether these vendors/consumers will eventually diversify their AI platforms with the MI300. This may also be made worse by NVDA’s aggressive launch of the next-generation GH200 Grace-Hopper superchip as a direct competitor to AMD’s MI300, scheduled for delivery in Q2 2024.

So while Lisa Su may have reported an increase in “AI cluster engagements by more than seven times sequentially”, it remains to be seen how much of this sampling can be successfully converted into orders and sales.

This is especially due to NVDA’s incremental supply of HGX every quarter until 2024, as similarly corroborated by Taiwan Semiconductor Manufacturing Company Limited’s (TSM) expanded CoWoS advanced packaging capacity for AI chips, from the original 8K monthly capacity. wafers in the first half of 2023 at 9K. in the second semester’23 and around 25K in 2024.

With AMD only securing a monthly capacity of 6K wafers in Q4 23, it seems that the Lisa Su-led company might be left behind in the early stage of the AI race. As a result, investors must also temper their short-term expectations accordingly.

So is AMD stock a buy?Sell or keep?

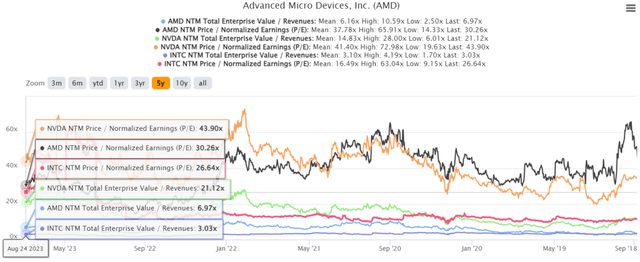

AMD 5-Year EV/Revenue and P/E Valuations

S&P Capital IQ

For now, AMD is trading at 6.97x NTM EV/Earnings and 30.26x NTM P/E, higher compared to its 5.67x/26.71x year-on-year average, though its P/E is still moderate compared to their pre-pandemic average of 4.31x/ 36.99x, respectively.

Most importantly, while AMD has historically traded close to NVDA’s valuations, we’ve already seen a drastic split since May 2021, with the latter taking the lead with a P/E NTM of 43.90x. This is due to the latter’s diversified chip and SaaS offerings in data center, AI, IoT, gaming and automotive end markets.

However, investors should note that AMD still commands a notable premium compared to semiconductor’s median P/E valuation of 19.32x, suggesting that it is not completely excluded from Mr. Market’s euphoria surrounding to generative AI.

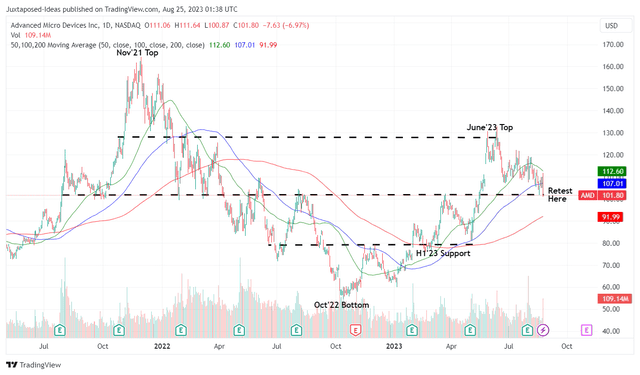

AMD stock price 2 years

commercial view

By now, AMD stock has recaptured much of its June 2023 gains and is currently retesting its August 2022/March 2023 $100 support levels.

It is clear that the exuberance surrounding generative AI has been too fast and furious, and many other related stocks, such as Super Micro Computer, Inc. (SMCI) and C3.ai (AI), have similarly pulled back in recent weeks. .

However, this is where opportunistic investors may consider adding, as the correction has generated further upside potential for our $160 long-term price target, based on AMD stock NTM P/E of 30.26x and Consensus FY2025 Adjusted EPS of $5.29.

We stand by our belief that while NVDA may have won the first round of the AI race, AMD is likely to share the spotlight in the long run, depending on the timing of their product releases.

For example, Lisa Su already hinted at her next-gen MI400 offerings in the recent earnings call, with a similar lineup scaled back for Chinese markets to comply with US trade policies, similar to NVDA’s H800 and A800 GPUs. :

China is a very important market for us, certainly across our portfolio, as we think about the accelerator market… We think there is an opportunity to develop products for our set of customers in China that are looking for AI solutions, and we will continue to work in that direction. (Looking for Alpha)

Combined with promising reports that the MI300 could outperform NVDA’s H100, we believe the total size of the $150 billion addressable AI chip market by 2028 is large enough to accommodate two winners.

As a result of the attractive risk/reward ratio, we continue to rate AMD stock a Buy for patient investors.

#AMD #Stock #Dont #Dismiss #Prospects #Race #NASDAQAMD