[ad_1]

jetcityimage/iStock Editorial via Getty Images

Introduction

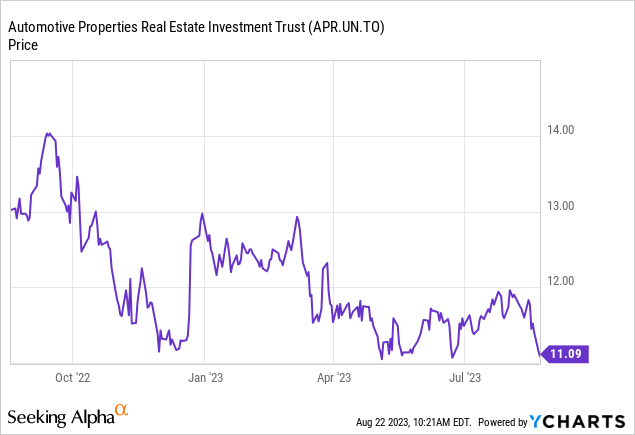

I started tracking the Automotive Property REIT (TSX:APR.UN:CA) in March of this year, as I was captivated by the well-covered dividend yield of 6.2%. Since that article was published, Automotive’s stock price has fallen 14% to its current level. of 11.15 Canadian dollars. This increases the distribution’s yield to approximately 7.2%. As the Canadian real estate sector has been quite volatile in recent weeks, I wanted to update my opinion on the REIT to see if this would be a good time to dive into the water.

There are currently 49.05 million units in circulation (including 9.3 million LP Class B units), resulting in a market capitalization of approximately C$547 million.

The FFO and AFFO results were decent.

To better understand Automotive’s business model and its exposure to its largest tenant (and largest shareholder), I’d like to refer you to my previous article. since March.

I was keen to see the financial performance of the REIT as it completed the acquisition of six properties in January of this year for a total acquisition cost of C$98.5 million. Acquisitions are triple net leases with a contractual rent increased based on the Quebec CPI, but with a minimum of 1.5%. The weighted average lease term was 16 years, so this acquisition provided excellent additional visibility to the REIT. While the top rate was not disclosed, auto properties were valued at about 6.75% at the time and I think that’s a fair assessment.

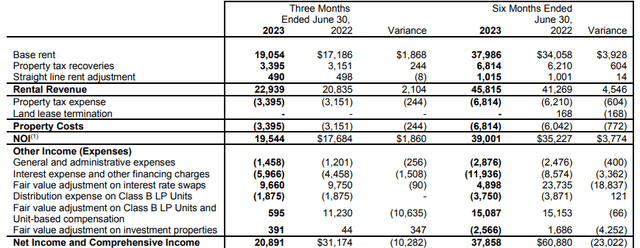

Turning to second quarter results, the REIT reported a total NOI of CAD 19.5 million, representing an increase of more than 10% compared to the second quarter of last year. Total NOI in the first half was C$39 million, which means that the annualized NOI is approximately C$78 million. An important metric, as real estate is valued at C$1.18 billion on the balance sheet, indicating a top rate of 6.6% and the NOI will obviously continue to rise thanks to contractual and inflation-related rent increases. .

APR Investor Relations

Obviously, the NOI is only one part of determining how attractive auto ownership is. The FFO and AFFO results provide a better indication and unfortunately higher interest expense meant that the total FFO and AFFO result was fairly flat.

APR Investor Relations

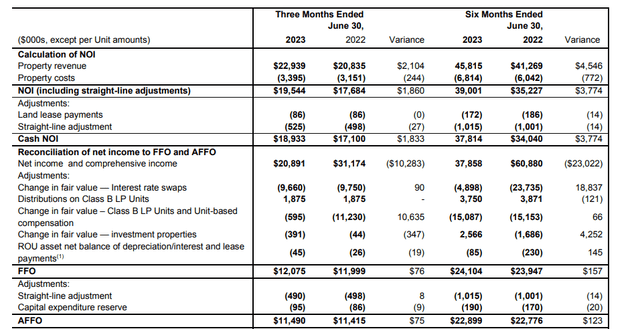

As you can see above, FFO was C$12.1 million in the second quarter of this year, compared to C$12 million in the second quarter of last year. And we see a similar increase in AFFO, which increased by C$75,000 to C$11.5 million. This means that the AFFO per share was approximately CAD 0.234. And based on the current distribution rate of 6.7 cents per month and therefore C$0.201 per quarter (and C$0.804 per year), the payout rate was 87.4% of AFFO. This means there is room for maneuver and the distribution is still well covered.

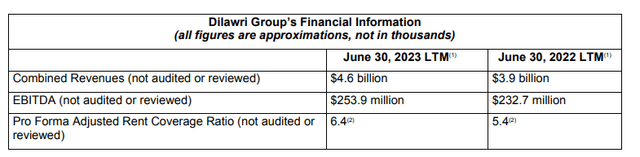

On an annualized basis, the stock is now trading at just under 12 times annualized AFFO. This is not unreasonable but of course the financial health of the main tenant, the Dilawri Group, is still very important, with Dilawri accounting for more than 50% of rental income so far this year. Fortunately, Automotive Properties provides a summary overview of Dilawri’s results. At the end of June, LTM EBITDA was approximately C$254 million, up from C$233 million at the end of the second quarter of last year. This also means that the pro forma adjusted rental coverage ratio increased from 5.4 to 6.4.

APR Investor Relations

Of course, a high EBITDA result does not necessarily mean that Dilawri is in excellent financial shape, but seeing strong EBITDA results is encouraging. And Dilawri obviously needs the real estate assets to carry out his daily activities.

As of the end of June, the REIT had about C$538 million in gross debt at a weighted average interest rate of 4.18%. The debt to gross book value ratio was approximately 45%. That’s up from 40% at the end of 2022, as most of the acquisition completed in the first half was covered by the credit line. Based on the current payout ratio, Automotive can retain around C$1.65 million from its AFFO on a quarterly basis. This equates to approximately CAD 6.5 million per year, which will help keep the debt ratio at an acceptable level and, at the same time, could help the REIT reduce its refinancing needs.

It goes without saying that the cost of debt will undoubtedly increase in the coming years, but I would expect Automotive Properties to increase the ratio of secured debt (mortgages) to the use of credit lines to keep the cost of debt in check.

A 200 bp increase in the average cost of debt (which would imply an interest rate of 6.18%) would increase the annual cost by C$11 million. Needless to say, that would be difficult considering it would drop AFFO/share by 22 cents per share to just over C$0.70.

But that’s why the rental escalators that exist today are so important. Assuming a 3% rent increase in 2024 followed by the minimum 1.5% rent increase in 2025, that would add about 7 cents per share. And because Automotive could reduce its net debt by C$15 million between now and the end of 2025 while keeping its dividend unchanged, it could reduce the impact by an additional 2 cents per share at the AFFO level.

investment thesis

This means that even in the worst case I don’t expect the REIT’s AFFO result to fall below 80 cents per share. In that case, the distribution would still be fully covered, although the coverage ratio would be too low to be comfortable.

This indicates that Automotive Properties could be attractive from an income standpoint, but I would not expect much in terms of capital gains in the coming years if interest rates in financial markets remain at their current level.

AFFO per share this year will probably be around C$0.92-0.93 and I expect some growth next year as 91% of interest exposure has been hedged, but rollovers from 2025 probably will affect the results, unless market interest rates will have decreased by then.

I don’t currently have any positions in auto properties yet, but the REIT offers exposure to an interesting niche while offering an attractive return.

#Auto #Property #REITs #Yield #Covered #TSXAPR.UNCA