[ad_1]

dragon claws

All values are in CAD unless otherwise noted.

We covered Killam Apartment REIT (OTC:KMMPF) in July of this year and got neutral sentiment on it. We liked the risk management and staggered debt maturities of This REIT is primarily apartments. Record immigration numbers in Canada turbocharged its net operating income, or NOI, helping it even outpace the interest rate hikes that hurt most companies’ bottom lines right now. Yielding around 4%, the REIT was selling at a slight discount to its NAV. We wanted to buy it at 14X FFO upfront and since it was trading above that, we gave it a pass. Today we will review another residential REIT to see if it passes the test, unlike Killam.

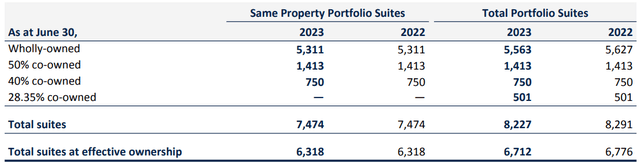

Minto Apartment Real Estate Investment Trust (TSX:MI.UN:CA) is a developer, owner and operator of multi-residential rental properties in Ottawa, Toronto, Montreal, Calgary and Edmonton. While the REIT co-owns a portion of its 31-property portfolio, the majority is wholly owned by it.

Q2-2023 MD&A

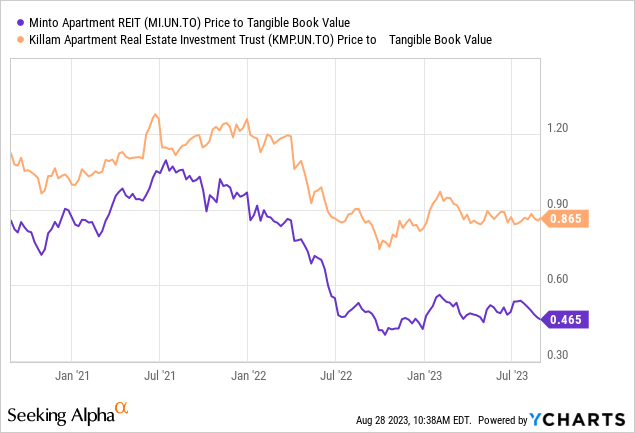

Minto distributes $0.04083 per month and, based on its current price of $13.21, returns its investors around 3.7%. Killam, on the other hand, yields slightly more at 3.9%, but not much. Both are trading at a discount, but Minto is comparatively a black sheep.

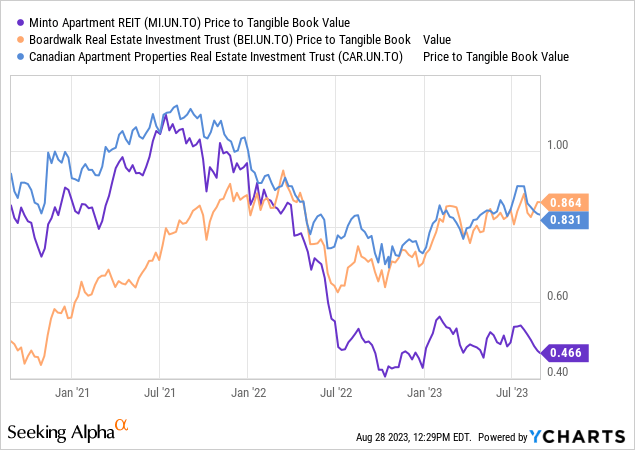

Minto fare similarly compared to the two giants in this space, Boardwalk Real Estate Investment Trust (OTCPK:BOWFF) (BEI.UN:CA) and Canadian Apartment Properties Real Estate Investment Trust (OTC:CDPYF) (CAR. A:CA). .

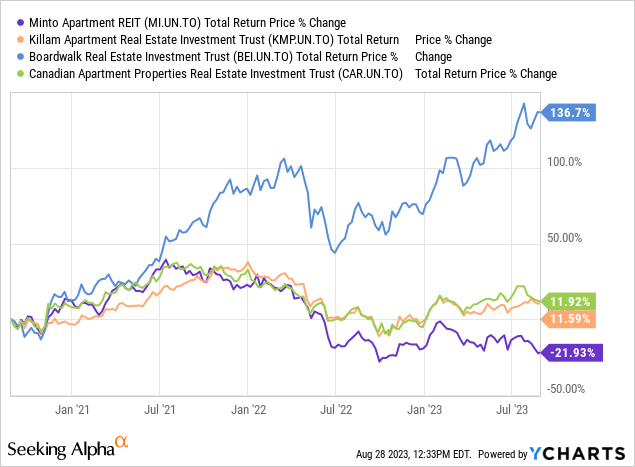

Another metric that reflects market contempt is the total price return over the last three years, compared to the aforementioned competitors.

We would be remiss if we went ahead with this article without giving a virtual high-five to Boardwalk sharers. In our opinion, the stock is overvalued, but that hasn’t stopped the monster move. Going back to Minto, the price drop more than made up for the elation its investors felt at its dividends over the past three years. With the immigration boom, why is Minto doing so much worse than its peers? Let’s see if the answers lie in recent financial results.

Q2-2023

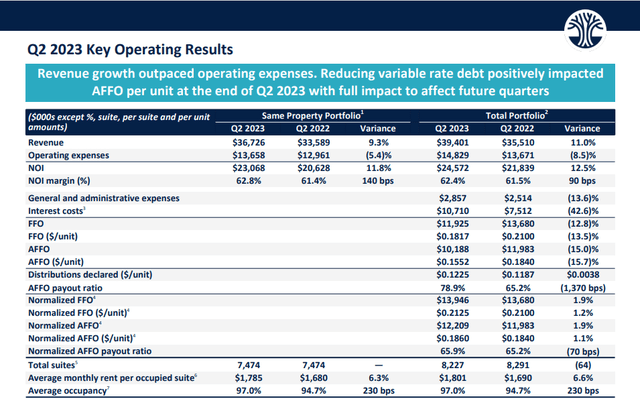

Cumulative acquisitions, an increase in average monthly rentals, lower turnover and increased occupancy levels contributed to year-over-year revenue growth of 11% for this REIT and its co-owners.

Presentation of the second quarter of 2023

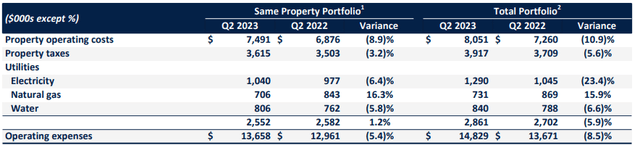

Lower inflationary pressures helped revenue growth to more than offset higher year-over-year operating expenses. A special shout out to the renegade among property-level expenses, natural gas. A double-digit drop in natural gas rates, combined with a warmer 2023, resulted in a healthy 16% decline in that spending.

Presentation of the second quarter of 2023

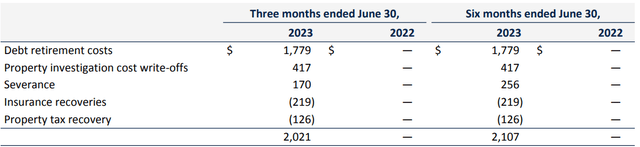

The overall result was a 12.5% higher net operating income or NOI compared to the second quarter of 2022. The 42% increase in interest costs was the main culprit for the 12.8% year-over-year decline. year in funds from operations or FFO. However, more than half of that increase came from non-recurring items.

Q2-2023 MD&A

Therein lies the difference between the change in simple FFO and normalized FFO, which was slightly positive. Both are shown in the first graph of this results section. Minto is working hard to reduce its exposure to variable rates, and debt retirement costs are part of that deal.

Presentation of the second quarter of 2023

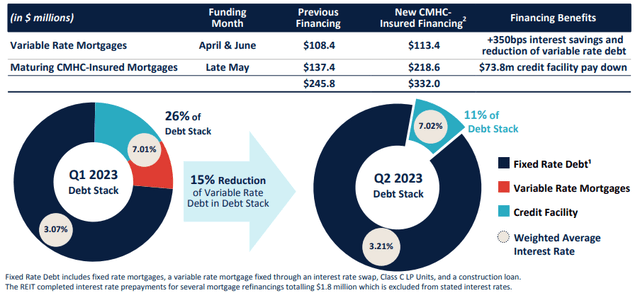

Minto addressed the magnitude and impact of these refinancings in its press release.

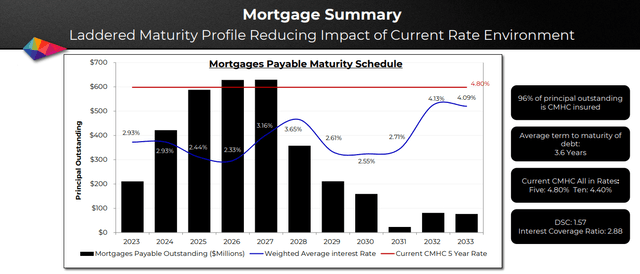

During the quarter, we refinanced seven mortgages with CMHC-insured long-term fixed-rate mortgages, reducing our variable-rate debt exposure from 26% of total debt to 11%, a reduction of more than $165 million. This also generated over $70 million of incremental revenue that we used to pay down our revolving credit facility (“Revolver”), which immediately increases FFO per unit. These initiatives only partially impacted the results for the second quarter of 2023, with the full increase occurring in the third quarter of 2023 and thereafter.

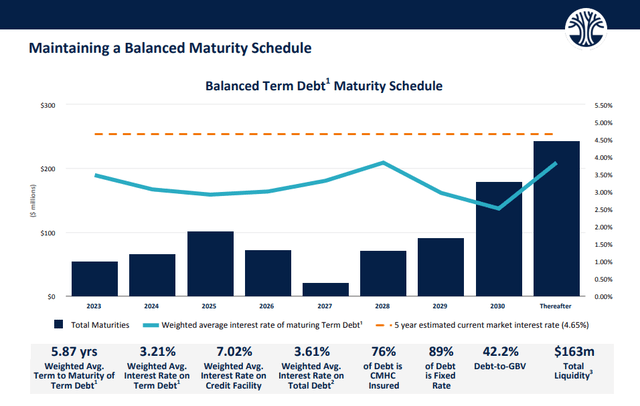

Debt service coverage ratio decreased from 1.66x at the end of 2022 to 1.48x at the end of Q2 2023 due to additional borrowing on its line of credit and higher rates on the line and rate debt REIT stock. Overall, while the rates it got on its second-quarter refinances were higher than its weighted average of 3.21%, the REIT made the right moves in light of the rates it was paying.

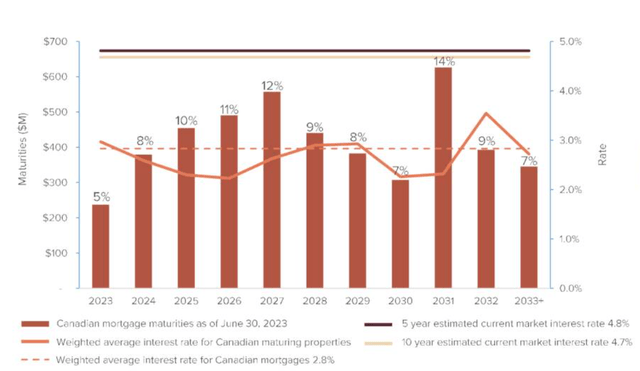

In April and June 2023, the REIT refinanced two variable-rate mortgages totaling $108.4 million with interest rates of 7.44% and 7.70% and secured $113.4 million in mortgages fixed-rate mortgages insured by CMHC with interest rates between 3.85% and 3.87% due in 2033. In May 2023, the REIT refinanced five overdue mortgages totaling $137.4 million with rates interest rates between 2.98% and 5.34% with $218.6 million of new fixed rate mortgages insured by CMHC with interest rates between 3.90% and 4.00%.3 which expire in 2028 and 2033.

Source: Press release

With CMHC’s blessings, Minto, like its siblings, enjoys lower-than-going rates, but still feels the impact of increases with each refinance.

Presentation of the second quarter of 2023

The weighted average interest rate of the term debt increased from 3.06% at December 31 to 3.21% at the end of the second quarter. We like the 5.87 year weighted average term to maturity on this REIT. By comparison, the CDPYF has an average maturity of 5.1 years, albeit with a lower weighted average interest rate.

Presentation CDPYF Q2-2023

Boardwalk, the superstar, has an average maturity of 3.6 years.

BOWFF Presentation Q2-2023

At 3.8 years old, Killam is closer to Boardwalk than to CDPYF and our protagonist. So compared to her peers, Minto comes out ahead in this regard.

Minto had around $163.3 million in liquidity at the end of the second quarter and was focused on increasing its cash flow per unit. It made some prudent capital decisions in light of that past quarter, deferring its planned intensification project on one of its properties and holding out on new development opportunities.

We believe our recent decisions to rescind the purchase option on the Fifth + Bank property, forgo three attractive development opportunities with Minto Properties Inc. (“MPI”), and delay the start of construction on the High Park Village addition demonstrate this approach. .

Source: Press release

Verdict

Minto is cheap and probably cheaper than ever. The market is valuing this REIT at a 5.5% capitalization rate, while the REIT believes its portfolio is just over 4%.

tikr

The gap to their consensus NAV is currently monstrous and we have a good degree of faith in this NAV.

Another residential REIT we like, Dream Residential Real Estate Investment Trust (DRR.U:CA) has an even larger discrepancy between implied and internally calculated NAV. We are bullish on the outlook and while in MINTO’s case the gap (difference between NAV cap rate and implied cap rate) is smaller, we still like it and rate it a Buy. A common theme for both is that we are getting a sufficiently large margin of safety and both have excellent debt profiles. The current market environment is tough for REITs, so the upgrade may not come instantly, but this looks like a buy candidate for anyone looking to buy quality apartment properties on the cheap.

Please note that this is not financial advice. It may look like it, it may seem like it, but surprisingly it’s not. Investors are expected to do their own due diligence and consult with a professional who knows their goals and limitations.

Editor’s Note: This article discusses one or more securities that are not traded on a major US exchange. Be aware of the risks associated with these stocks.

#Minto #Apartments #Attractively #Priced #Residential #REITs #TSXMI.UNCA