[ad_1]

welcome inside/iStock via Getty Images

In the years that I have followed the oil market, I have never seen the Saudis so intent on pushing up oil prices. This includes the “whatever it takes” moment we saw in 2017, when former Saudi energy minister Khalid Al-Falih began attacking US inventories and the 2020 price war as the Saudis came out to crush the Russians for not accepting a production cut.

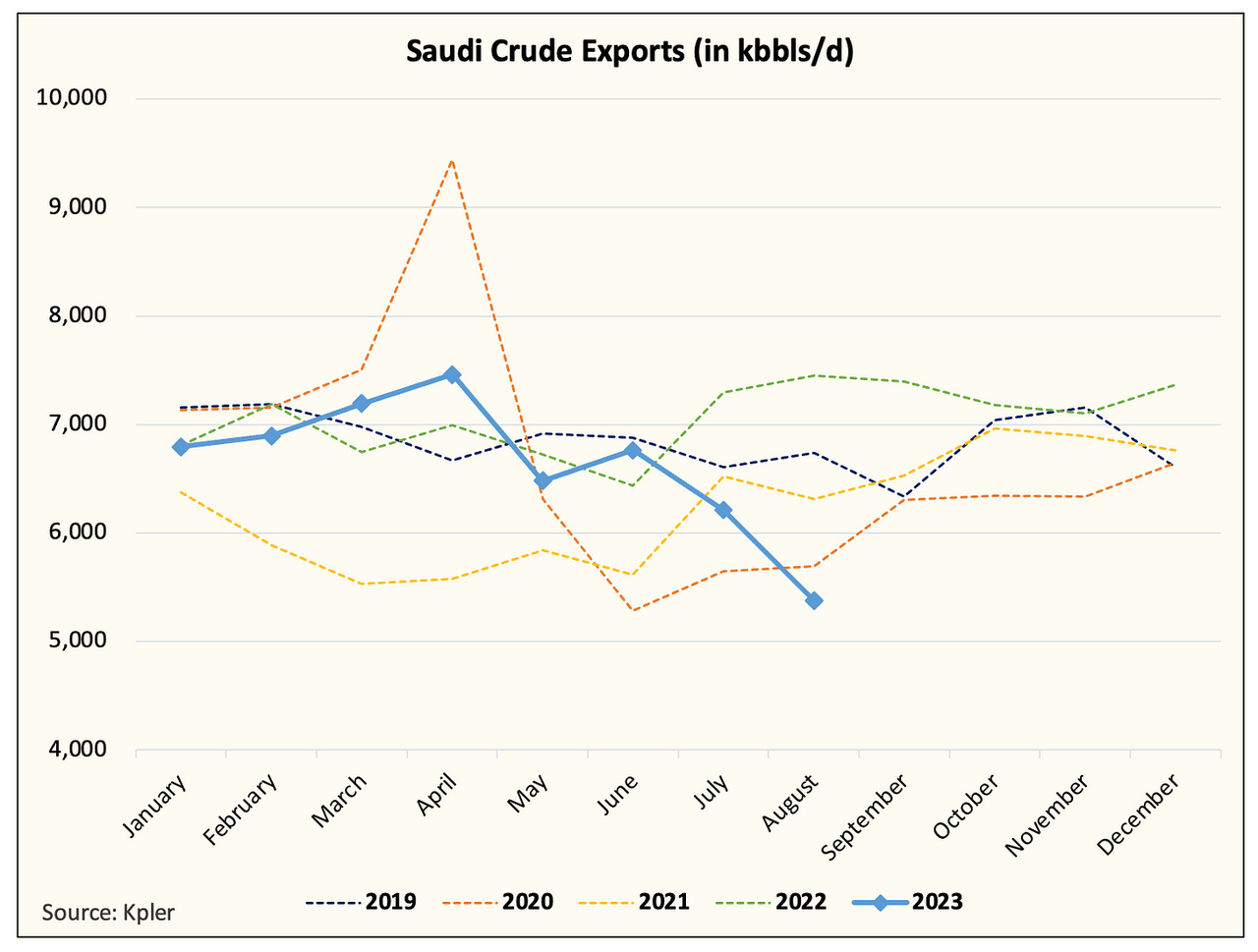

Kpler

Saudi crude oil exports for the first 24 days of August are on average at the lowest level since June 2020. At ~5.3 million b/d, the Saudis will have reduced crude exports by ~1 million b/d /d since July. However, we do not expect this figure to be definitive. Crude exports for the next week are showing a rebound, so the final numbers could be closer to 5.6 to 5.8 million b/d.

but not that Please change the point of this article, this is crazy, and I have never seen the Saudis so determined.

Those of you who follow us closely will know that our basic vision is for the Saudis to extend the voluntary cut until the end of the year. We explain that it is due to the logistical timing issue of when exports affect physical inventories and the impact on market sentiment. But with the latest Saudi crude export figure, I can’t help but wonder if the cut is likely to extend into the first quarter of 2024.

Let me explain.

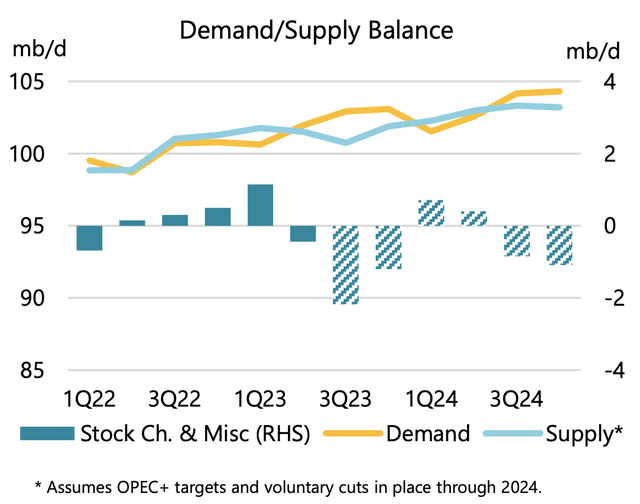

IEA

Here’s the IEA’s assumption of the global balance between oil supply and demand through the end of 2024. Of all the IEA reports we’ve read to date, the August OMR was the most balanced (surprising).

You will now notice that both the first and second quarters of 2024 show stock increases. Note that the IEA does not assume the voluntary cut of ~1 million b/d on its balance sheet in 2024. Instead, it assumes that the Saudis will continue with their original voluntary cut of ~500,000 b/d.

In my opinion, the Saudis played wonderfully. By keeping it month to month, it discourages speculators from bidding higher on the long end of the curve and keeps the market in check. The monthly action also prevents speculators from taking advantage of prices, preventing any potential risk of demand destruction amid a weak global economy. Instead, the voluntary cut serves the only purpose it was meant to serve: to reduce global inventories.

Now imagine this scenario: As we approach the end of October, oil continues to trade in the $80 to $90 range. Although world oil inventories have been substantially depleted, confidence remains weak and speculators believe that the impending recession will affect oil demand. The Saudis are now deciding whether to extend the period until the end of December, but looking at global oil supply and demand balances, the first quarter shows an increase. All voluntary cutting efforts up to that point would be for naught if storage increases again.

With the voluntary cut already in place, what’s to stop the Saudis from slowly phasing out the cut? Perhaps best after Q1 to slowly taper off the ~1m b/d cut to avoid any inventory buildup. Also, with Russia cooperating (finally), and if the Russians extend their voluntary cut until the end of the year, then it will be physically very difficult for Russia to ramp up production through the dead of winter. All these things suggest to me that there is a greater than 50% chance that the Saudis will extend this voluntary cut (in some form) until the end of the first quarter and possibly the second quarter of 2024.

Now this is not the consensus view and many of the oil analysts expect the Saudis to ease the voluntary cut once the storage reduction has materialized, but we digress. We think the ultimate goal of the Saudis is price stability, so if that implicitly implies an overall lower level of storage to achieve that, then the Saudis will keep the voluntary cut until they see fit.

This means that Brent would have to easily average over $90 for many months before the Saudis contemplate a reduction. We just don’t see that when the consensus expects a first quarter rise.

This is crazy…

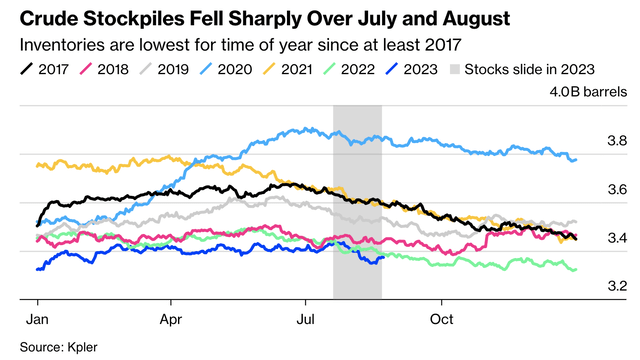

Kpler

In the years that I have followed the Saudis, this is the most determined occasion that I have seen them. If we’re right and the Saudis continue to spread, then the market is in for a rude awakening. Global onshore crude oil inventories are already starting to accelerate downward and there is more to come. Perhaps, like the article we published on Monday, it really is that simple. Maybe it’s not. We will know in time.

Editor’s Note: This article covers one or more micro-cap stocks. Be aware of the risks associated with these actions.

#Saudis #pushing #oil #prices #CommodityCL1COM